Are record Spotify Earnings enough to offset a sharp stock plunge after management’s surprisingly cautious Q2 outlook?

How are Spotify Earnings hitting the stock today?

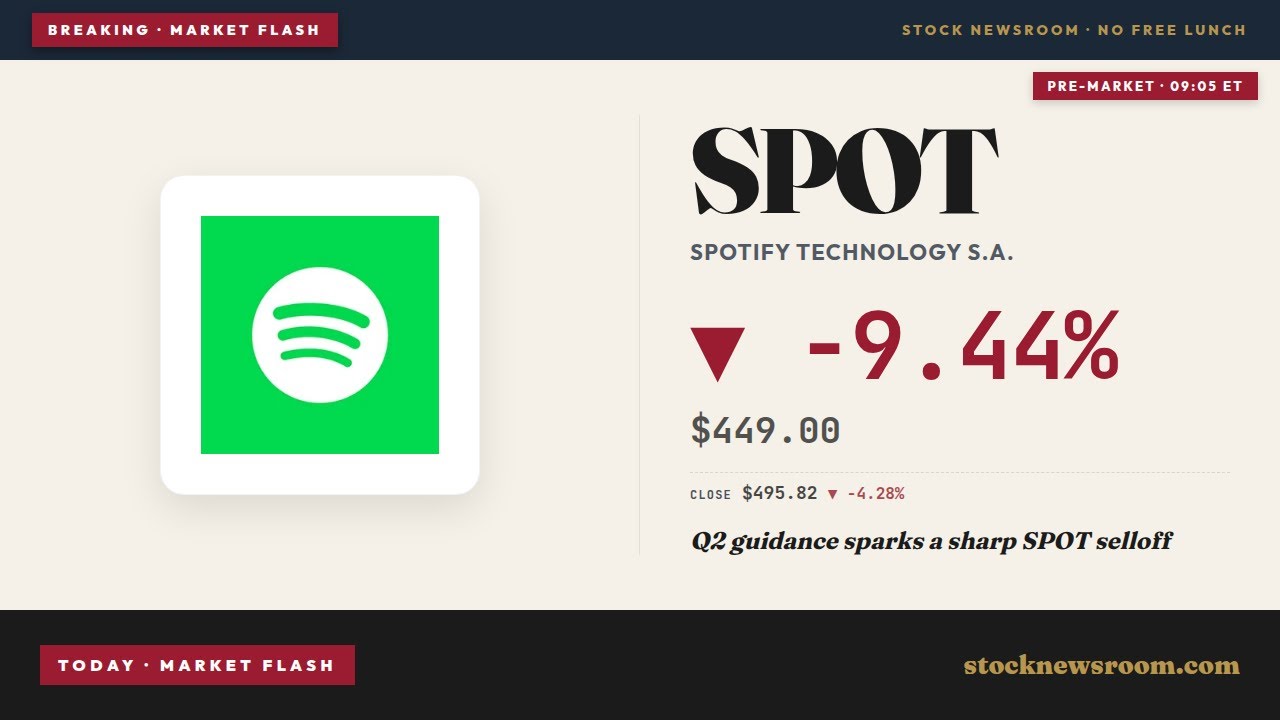

Before the opening bell on Tuesday, SPOT traded around $450, down roughly 9% from Monday’s close of $498.60. That follows a 4.28% loss in the prior session, leaving the stock about 15% lower year to date and more than 30% below its 2025 highs. At Monday’s close the stock still changed hands near $495.82, implying a premium multiple that gives little room for guidance disappointments.

The selloff comes even though Q1 2026 Spotify Earnings delivered precisely what many bulls had hoped for: record profitability, expanding margins, and continued scale. Operating income jumped to a record EUR 715 million, rising about 40% year over year and easily topping consensus. Net income more than tripled to EUR 721 million, aided by EUR 222 million in finance income and a EUR 216 million tax benefit, while free cash flow surged 54% to EUR 824 million.

Revenue reached about EUR 4.5 billion, up 8% as reported and 14% on a constant-currency basis, roughly in line with expectations. Premium revenue grew double digits, supported by price hikes in key markets like the United States, where the standard Premium plan now costs $13 per month. Importantly, churn remained low, suggesting that users are reluctant to leave behind long-curated playlists and recommendations even as prices rise.

What do the Spotify Earnings say about user growth?

On the user front, Spotify Technology S.A. continued to show scale advantages that most rivals can only envy. Monthly active users climbed 12% year over year to 761 million, edging past Wall Street expectations of about 759 million. Paying subscribers rose 9% to 293 million, adding 3 million premium accounts during the quarter and matching analyst estimates.

The company expects to continue that momentum into Q2, guiding to 778 million monthly active users and 299 million premium subscribers. That implies an additional 6 million paying customers in a single quarter, a pace that still positions Spotify ahead of many entertainment peers. While YouTube, Amazon Music and services from Apple and Meta compete aggressively in music and audio, none combine Spotify’s scale with its personalized recommendations engine and breadth of podcasts, audiobooks and, now, fitness content.

Advertising revenue remains a smaller but increasingly strategic piece of the model. Ad-supported revenue declined about 5% on a reported basis, but management pointed to a roughly 3% gain excluding currency effects, driven by stronger music ad impressions and improving podcast sponsorships. For U.S. investors watching the broader digital ad cycle at companies like Meta and NVIDIA’s AI-driven ad infrastructure partners, this modest rebound is a positive signal but not yet a major earnings driver.

Why did the Q2 outlook disappoint?

The pressure on SPOT shares stems from guidance, not the Q1 print. Management projected Q2 operating income of EUR 630 million, below the EUR 684 million Wall Street had penciled in. Revenue is expected around EUR 4.8 billion, with continued user and subscriber growth but less margin upside than many had hoped for in what Spotify has branded the “Year of Raising Ambition.”

Part of the Q1 profit strength came from lower payroll-related social charges, which move with the company’s own stock price. With SPOT down in 2026, those costs dropped and temporarily boosted margins, a tailwind that is unlikely to repeat at the same scale in Q2. That normalization, combined with ongoing content investments and product expansion, helps explain why the Q2 operating income outlook underwhelmed.

Analysts who had recently turned more constructive on Spotify Earnings now face a tougher narrative to defend. Research from firms like GuruFocus highlighted upgrades to “Buy” on the back of rising margins and the potential for gross margins to exceed 35% by 2028, but today’s reaction suggests investors want clearer evidence that those long-term targets are intact even as near-term costs normalize.

How do Peloton and AI fit into the growth story?

Strategically, Spotify is pushing beyond audio into broader engagement. The company just launched a new fitness category through a partnership with Peloton, unlocking more than 1,400 ad-free workout and wellness classes for Premium subscribers worldwide. While the financial terms are undisclosed, the collaboration gives Peloton reach into Spotify’s nearly 300 million paying users and helps Spotify add stickier use cases beyond music and podcasts.

Investors are still debating whether this “Spotify Fitness” push can move the needle or is more of a marketing add-on. The deal has already boosted Peloton’s stock, but SPOT has slipped as traders await proof that fitness engagement translates into higher retention or pricing power. For comparison, Tesla and other consumer-tech brands have shown that layered subscription features can support valuations; Spotify is trying to replicate that playbook in media.

The other big open question is artificial intelligence. Wall Street remains skeptical about whether Spotify can carve out a defensible AI strategy while competing with giants like YouTube, Amazon and Meta that are deeply embedded in AI research and infrastructure. Spotify is experimenting with AI-powered playlist creation, more controllable recommendations and integrations on platforms like ChatGPT and Claude, but the market has yet to see a breakthrough feature that clearly monetizes AI or differentiates Spotify in the NASDAQ tech ecosystem.

Related Coverage

For a deeper dive into how the Peloton partnership might reshape the narrative, readers can explore “Spotify Fitness -3.9% Plunge: Can Peloton Power Growth?”, which examines whether fitness content can offset recent share-price weakness and support the next leg of growth for SPOT.

All that reinforces our confidence in sustained user and subscriber growth, low churn, and continued progress on revenue and margin.— Alex Norström, Co-CEO of Spotify Technology S.A.

In summary, the latest Spotify Earnings underscore a company that is finally delivering sustained profitability but still struggling to convince Wall Street about the durability of that trend. For U.S. investors, the mix of record margins, ongoing user growth and a cautious Q2 outlook makes SPOT a high-beta play on global streaming, AI-enhanced personalization and subscription pricing power. The next few quarters of Spotify Earnings will be crucial in proving whether this dip is a buying opportunity or an early warning that growth and margins are peaking.