Why is Applied Digital Data Center stock sliding hard just as billion-dollar hyperscaler leases and AI campus expansion hit the tape?

What’s Driving the Applied Digital Data Center Expansion?

Applied Digital Corporation has transformed from a Bitcoin miner into a vertically integrated AI infrastructure provider — and its latest milestones underscore that pivot. On July 1, 2026, the company completed Building 2, Phase 1 at Polaris Forge 1 in North Dakota, adding 75 MW of AI-optimized power capacity. The campus now operates at 175 MW, with a fully contracted target of 400 MW. CEO Wes Cummins described the repeatable deployment model as an ‘AI Factory’ — emphasizing speed, scalability, and power-density advantages over legacy data centers. This isn’t theoretical: the company now counts five signed leases with high-investment-grade U.S. hyperscalers — including three with the same unnamed client, signaling deepening trust in Applied Digital’s execution. The infrastructure is purpose-built for GPU-intensive workloads, directly competing with offerings from NVIDIA-aligned providers like CoreWeave and StackPath — but with a North American onshoring edge that resonates with defense and enterprise AI buyers.

How Big Is the New Hyperscaler Deal?

The newly announced 210 MW lease at Delta Forge 2 — slated for a Southern U.S. state — carries staggering financial weight. Base revenue commitments total $5.2 billion over 15 years, with extension options pushing total potential value to $12.7 billion. That deal alone represents more than 3.5x Applied Digital’s current market cap. To fund the buildout, the company secured a $550 million credit facility from Goldman Sachs and issued a $1.59 billion project-specific bond — both structured to align with long-term cash flow visibility. Notably, the contract includes robust uptime SLAs and power reliability guarantees — features that distinguish Applied Digital Data Center assets from generic colocation providers. For Wall Street, this isn’t just revenue; it’s de-risked, inflation-linked, investment-grade cash flow — a rare profile in the NASDAQ’s AI infrastructure cohort.

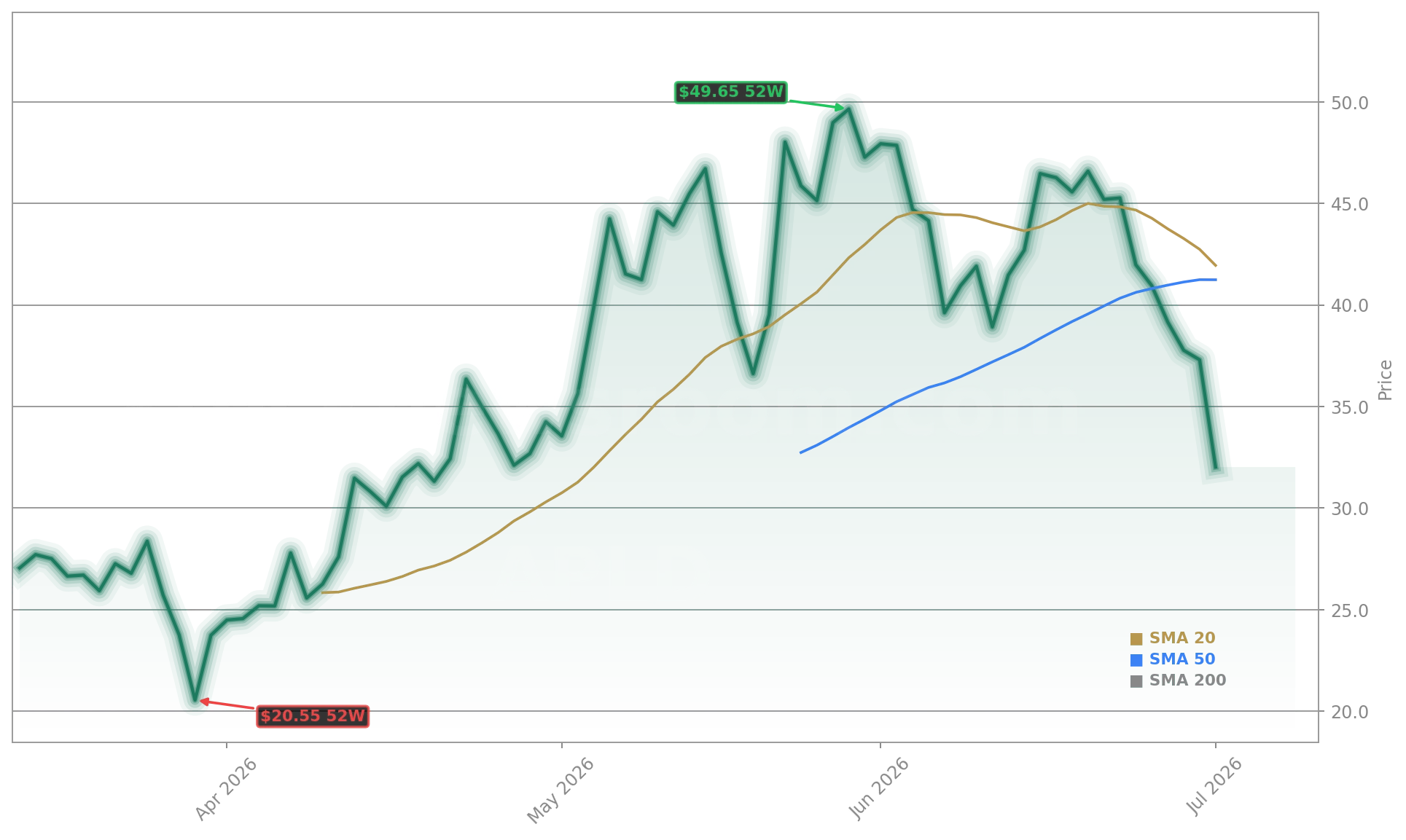

Why Is the Stock Falling Despite Record Progress?

APLD’s 9.71% drop on Thursday — to $32.07 from $35.52 — reflects short-term skepticism, not long-term rejection. The stock is down nearly 20% in one week and over 30% month-to-date, even as RSI dips to 32 — approaching oversold territory. Analysts aren’t backing down: Northland Capital Markets raised its price target to $82 and reaffirmed an Outperform rating, citing ‘exceptional execution by management, site sourcing, and development teams.’ Craig Hallum lifted its target to $79 from $75 and reiterated a Buy, highlighting the 109% upside potential. B. Riley also maintains a Buy at $66. The disconnect stems from timing: investors are pricing in near-term construction cost overruns, interconnection delays, and broader AI stock rotation — especially as memory plays like SanDisk face pressure. Yet Applied Digital’s contracted revenue base now dwarfs peers like CoreWeave (private) and even public competitors such as Switch (SWCH) on a per-MW revenue basis.

How Does This Fit Into the Broader AI Infrastructure Landscape?

Applied Digital Data Center growth comes amid a structural shift in AI infrastructure sourcing. With U.S. export controls tightening and federal AI procurement mandates accelerating, hyperscalers are diversifying away from overseas GPU clusters — and Applied Digital is one of only two NASDAQ-listed companies with live, multi-hundred-MW AI campuses under contract. Its model bypasses traditional cloud capex cycles by offering dedicated, pre-integrated GPU racks with 100% power redundancy. That puts it in direct dialogue with infrastructure demands from Tesla and Apple, both of which are scaling on-premise AI training capacity. While companies like Equinix (EQIX) and Digital Realty (DLR) expand AI-adjacent offerings, Applied Digital’s focus on GPU-native power and cooling gives it a defensible niche — one that Northland explicitly calls ‘the most scalable AI infrastructure platform in North America.’

What’s Next for Applied Digital’s Growth Trajectory?

Our AI Factory model delivers predictable, scalable, and power-optimized infrastructure — exactly what hyperscalers need as they confront GPU supply constraints and latency requirements.— Wes Cummins, CEO of Applied Digital Corporation

Delta Forge 2 construction begins in Q3 2026, with first capacity expected online by Q1 2027. Meanwhile, Polaris Forge 1’s remaining 225 MW will come online in two phases through mid-2027. Applied Digital also confirmed plans to launch Delta Forge 3 in late 2026 — targeting a new industrial corridor with sub-3.5¢/kWh power. With $1.4 GW of contracted capacity already secured and over $18 billion in total potential revenue across its pipeline, the company is shifting from growth story to cash flow story. Next quarter’s earnings report will be the first to reflect meaningful revenue from the new Polaris Forge 2 units — a critical catalyst for re-rating.