Has BlackBerry finally found a credible turnaround story, or is this post-earnings surge getting ahead of itself?

What Did BlackBerry Earnings Reveal?

BlackBerry Limited reported Q1 2026 adjusted earnings per share of $0.04, exceeding the $0.03 average analyst estimate compiled by Bloomberg. Revenue came in at $162 million, broadly in line with expectations, but the standout metric was operating cash flow: $12.3 million positive—its first such quarterly outturn since Q1 2017. This inflection point underscores the company’s successful pivot toward high-margin software licensing, particularly through its QNX platform embedded in over 250 million vehicles globally. Unlike legacy peers, BlackBerry no longer relies on hardware sales; instead, its automotive software, cybersecurity services, and embedded systems licensing now generate over 85% of total revenue. The strong cash generation validates management’s capital discipline and sets the stage for increased R&D investment in AI-enhanced threat detection tools for autonomous systems.

Why Did Wall Street React So Strongly?

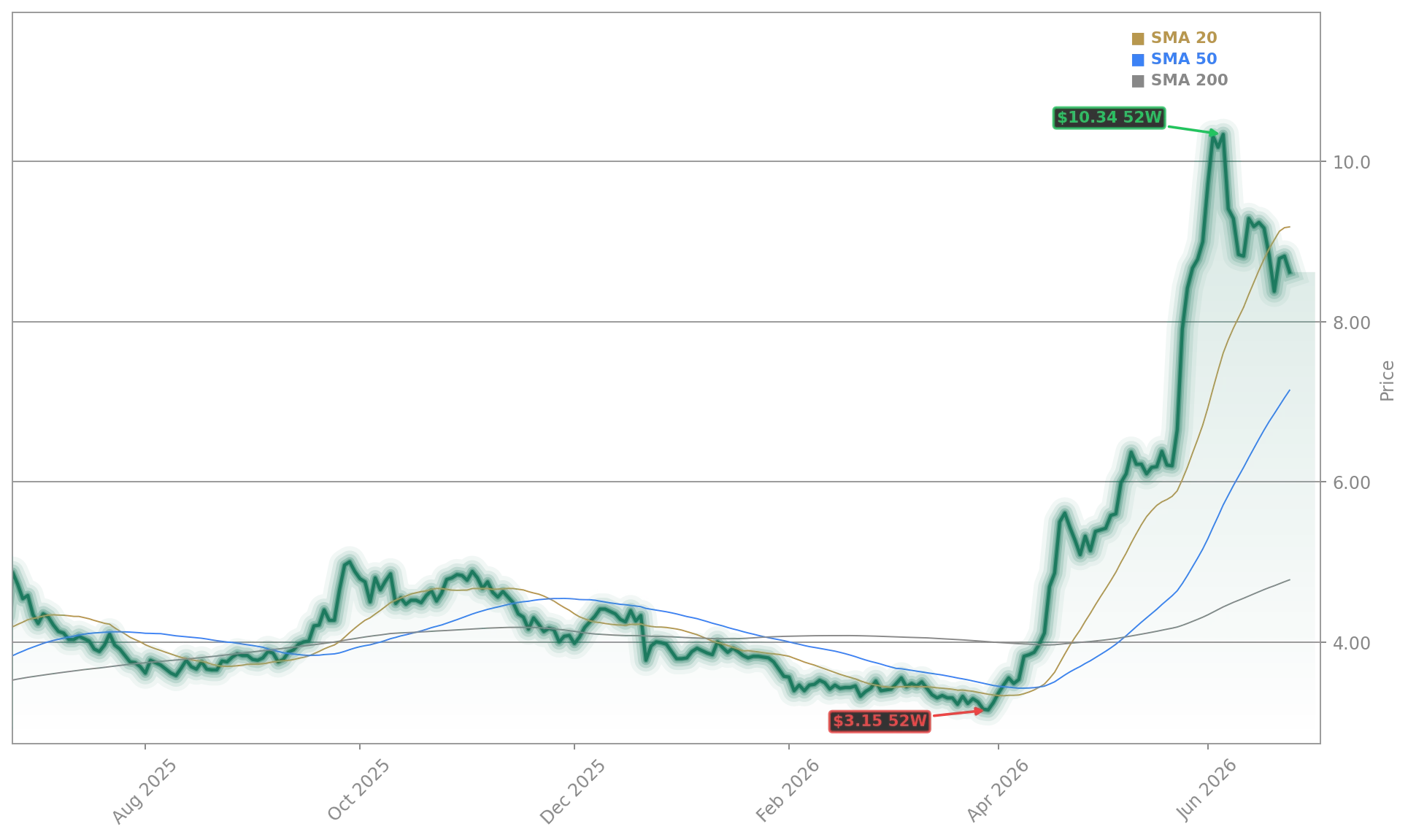

The 21.8% intraday surge in BB shares—lifting the stock to $10.50 from $8.62—reflects more than just a beat. It reflects investor reassessment of BlackBerry Limited’s strategic relevance in two critical S&P 500-adjacent growth vectors: automotive software and AI-powered security. While NVIDIA dominates AI chip infrastructure and Tesla leads vehicle electrification, BlackBerry’s QNX remains the de facto real-time OS for ADAS and autonomous driving stacks across Toyota, Mercedes-Benz, and General Motors. Analysts at RBC Capital Markets upgraded BB to ‘Outperform’ with a $13.50 price target, citing ‘underappreciated optionality in AI-augmented endpoint security and regulatory tailwinds from U.S. EV cybersecurity mandates.’ The stock’s rally also contrasts sharply with broader NASDAQ volatility—where the index dipped 0.3% on the same day—highlighting BB’s idiosyncratic catalyst strength.

How Does BlackBerry Earnings Compare to Peers?

Unlike hardware-dependent peers such as BlackBerry’s former handheld rivals, today’s BlackBerry Earnings performance aligns more closely with high-visibility software infrastructure names like Apple—which reported 18% YoY services revenue growth last quarter—or Palo Alto Networks, whose cybersecurity licensing model shares structural similarities. Crucially, BB’s gross margin of 89% in Q1 2026 surpasses industry averages for enterprise software (typically 75–85%) and even exceeds Palo Alto’s 82%—a reflection of QNX’s embedded, low-touch delivery model. This margin advantage enables BB to fund R&D without dilution: no new equity was issued in Q1, and net debt declined by $24 million year-over-year. In contrast, peers like Qualcomm and Marvell reported solid chip demand but face margin pressure from AI memory supply constraints—making BlackBerry Limited’s software-led resilience especially notable amid semiconductor volatility.

What’s Next After This BlackBerry Earnings Report?

Management raised its fiscal 2027 revenue guidance to $670–$690 million (up from $650–$675 million) and now expects non-GAAP EPS of $0.16–$0.19, a 25% increase at the midpoint. The revised outlook assumes accelerated adoption of BlackBerry IVY—a cloud-connected vehicle data platform co-developed with Amazon—and expanded contracts with Tier 1 automotive suppliers. Near-term catalysts include Q3 2026 certification of QNX AI Guard for ISO/SAE 21434 compliance, potentially unlocking $150+ million in new federal and EU government contracts. Citigroup affirmed its ‘Buy’ rating and lifted its 12-month price target to $12.80, stating: ‘BB’s path to $12 is no longer speculative—it’s a function of execution on embedded AI monetization.’ With the stock trading at just 3.8x forward sales—well below the S&P 500 software sector median of 7.2x—valuation remains a key upside lever.

BlackBerry Earnings: What Should Investors Watch Now?

BB’s path to $12 is no longer speculative—it’s a function of execution on embedded AI monetization.— Citigroup

While the Q1 2026 BlackBerry Earnings report delivered a clear beat, forward momentum hinges on two near-term metrics: QNX design-win velocity in L3+ autonomous systems and IVY platform monetization traction. Investors should monitor Q2 2026 disclosure of new customer logos—especially in commercial EV fleets and U.S. defense contractors—as leading indicators. The company’s $200 million strategic investment in AI threat modeling, announced in April, also ties directly to the expanded BlackBerry Nvidia Partnership Sparks New AI Boom Warning|https://stocknewsroom.com/blackberry-nvidia-partnership-ai-boom-warning/—a development that could accelerate licensing revenue from AI-augmented endpoint security. Meanwhile, AMC’s recent $200 million debt offering reshapes the broader tech-adjacent capital markets landscape, reinforcing investor appetite for cash-flow-positive, non-dilutive growth stories like BlackBerry Limited.