Does TTRF Capital’s massive Nebius Stake signal the next AI infrastructure winner, or a valuation warning investors should not ignore?

Who Just Took a Major Nebius Stake?

TTRF Capital Ltd disclosed a new position in Nebius Group on July 6, 2026, via an SEC 13F filing—valued at $64.0 million at quarterly average pricing and swelling to $89.2 million by quarter-end. The stake now represents 58.8% of TTRF’s reported 13F assets, marking the firm’s largest single equity commitment. This move follows Nebius Group’s August 2024 rebrand from Yandex N.V. and arrives as the company executes on multi-year infrastructure build-outs. Unlike passive index funds, TTRF’s concentrated bet signals conviction in Nebius’ role as a foundational AI infrastructure provider—not just a cloud vendor. The firm’s portfolio includes just 13 equity positions, making the Nebius Stake a strategic anchor rather than a tactical trade.

What’s Driving Nebius’ Revenue Surge?

Nebius Group’s Q1 2026 revenue hit $399 million—up 684% year over year—fueled primarily by long-term contracts with hyperscalers. Most notably, Meta signed two separate five-year agreements totaling $27 billion earlier this year, accelerating revenue recognition from previously committed capacity. That deal dwarfs prior engagements and reflects Meta’s urgent need for GPU-dense, low-latency infrastructure to train next-gen foundation models. Nebius’ AI cloud platform now delivers over 1.2 exaFLOPS of compute—comparable in scale to mid-tier offerings from NVIDIA-powered cloud partners. Yet revenue growth remains lumpy: 841% YoY AI Cloud revenue growth masks an underlying $100.3 million adjusted net loss—20% wider than Q1 2025—due to ongoing data center construction and lease obligations totaling $9.9 billion.

How Does Nebius Stack Up Against Wall Street Peers?

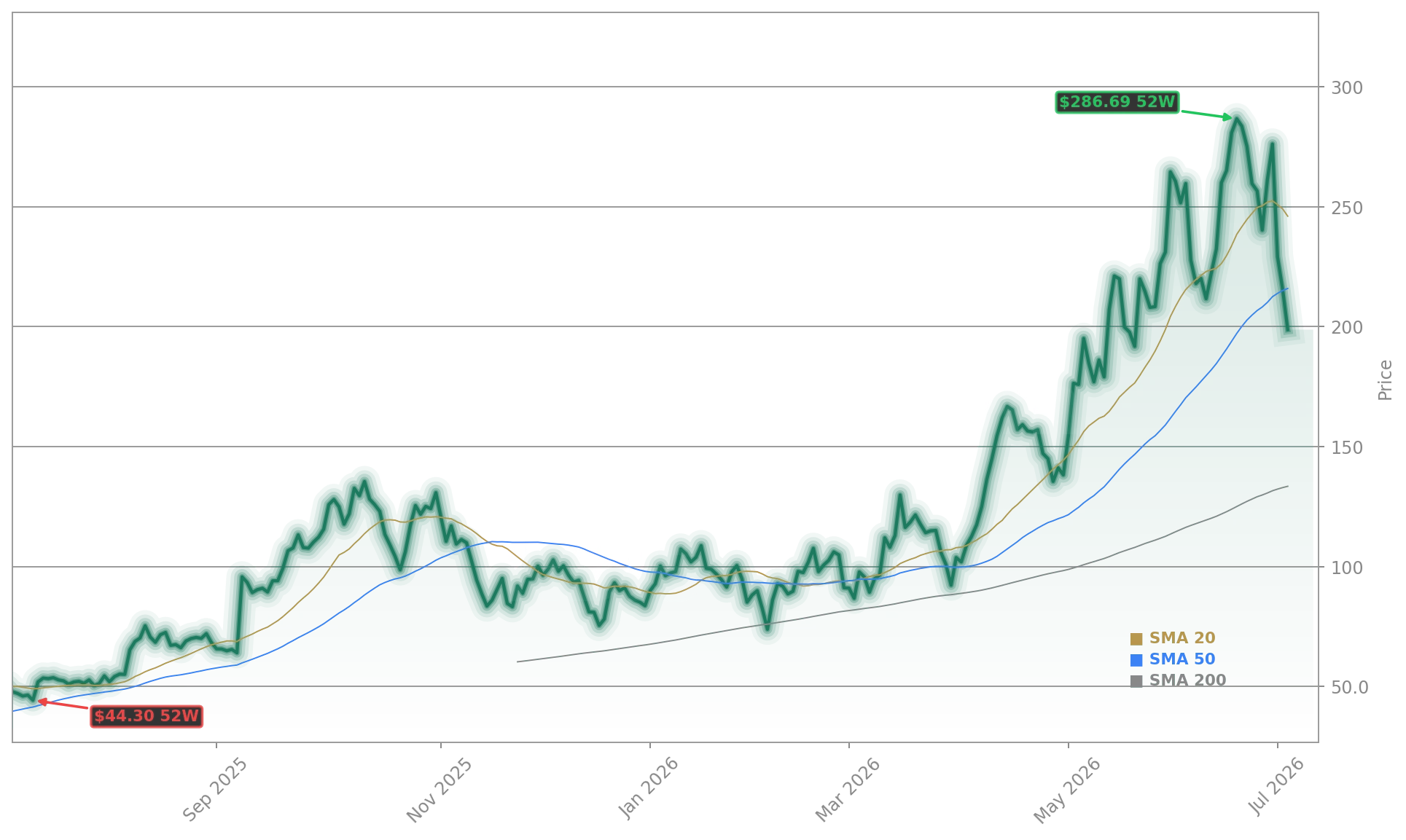

Valuation metrics reveal a stark contrast with established tech leaders. Nebius trades at a forward P/E of 68 and a price-to-sales ratio of 62—versus Meta’s forward P/E of 19 and $44 billion in annual free cash flow. Morningstar assigns a fair value estimate of $120—nearly 40% below Monday’s $200.43 close. Meanwhile, Citigroup maintains a ‘Neutral’ rating on Nebius with a $165 price target, citing execution risk in scaling power delivery and cooling infrastructure across Amsterdam, Dallas, and Tel Aviv. RBC Capital Markets recently downgraded the stock to ‘Underperform’, warning that rising interest rates could pressure Nebius’ $10.04 billion in convertible debt. By comparison, Apple and Tesla have leveraged AI infrastructure investments to boost margins—not dilute them.

Is the Nebius Stake a Signal or a Distraction?

The $89.2 million Nebius Stake is more than a headline—it’s a litmus test for institutional appetite in pre-profitability AI infrastructure plays. While TTRF’s move echoes early bets on cloud pioneers like AWS pre-2010, today’s environment is far more competitive. Microsoft Azure and Google Cloud are expanding AI-optimized regions at record pace, and Meta’s own cloud monetization plans—announced in May—add direct competitive pressure. Still, Nebius’ diversified model (Toloka AI, TripleTen, Avride) offers cross-selling leverage most pure-play infrastructure firms lack. The company’s 4-gigawatt contracted power target by year-end would position it as the third-largest AI-dedicated power buyer globally—behind only Google and Microsoft. That scale may attract further Nebius Stake interest from infrastructure-focused funds like BlackRock’s iShares Global Infrastructure ETF, which added $210 million in AI data center equities last quarter.

What’s Next for Nebius and Its Institutional Backers?

Nebius’ ability to convert committed power into billable uptime—not just signed contracts—will define its credibility in 2026.— Goldman Sachs analysts

With Q2 2026 earnings due August 12, Wall Street will focus on three metrics: gross margin expansion (currently 22%), lease obligation disclosures, and progress on its first U.S.-based AI cluster in Texas. Goldman Sachs analysts note that ‘Nebius’ ability to convert committed power into billable uptime—not just signed contracts—will define its credibility in 2026.’ The firm maintains a $180 price target and ‘Hold’ rating. Meanwhile, the Nebius Stake by TTRF has already triggered follow-on interest: two U.S.-based hedge funds filed preliminary 13D notices last week, signaling potential activist engagement around capital allocation. For investors, the core question remains: Is Nebius a strategic infrastructure play—or a high-risk, high-volatility proxy for AI hype? The answer may hinge less on quarterly growth and more on how quickly it turns megawatts into margins.