Can blockbuster AMD Earnings and a surging AI data-center business really justify the stock’s latest double-digit rally?

How strong were AMD Earnings this quarter?

AMD delivered a standout quarter that underscored the strength of its AI and data-center strategy. Revenue for Q1 2026 climbed to about $10.25 billion, up roughly 38% year over year and comfortably ahead of Wall Street estimates near $9.9 billion. Adjusted earnings per share reached $1.37, rising more than 40% and confirming that AMD is not just growing, but doing so profitably.

The highlight was the data-center segment, which has become the company’s primary growth engine. Data-center revenue surged to $5.8 billion, a roughly 57% jump from the prior year and a clear acceleration from the mid‑30% growth pace seen late in 2025. This unit combines AMD’s EPYC server CPUs with its Instinct AI accelerators, both manufactured on advanced process nodes at TSMC, and is now the strategic core of the AMD Earnings story.

Other divisions contributed as well. Client and gaming revenue increased around 23%, benefiting from renewed PC demand and console upgrades, while the embedded business returned to growth with a mid‑single‑digit gain. Still, data center and AI are setting the tone for how Wall Street values AMD.

What is driving AMD’s AI momentum?

The current AMD Earnings cycle is closely tied to a massive global AI investment wave. Hyperscale cloud providers are collectively deploying well over $200 billion into AI infrastructure, and while NVIDIA still holds an estimated 80% share of the accelerator market, AMD is emerging as a crucial second source. Its Instinct accelerators and EPYC CPUs, together with rack‑scale Helios systems slated to ship later this year, offer cloud giants a way to diversify away from single‑vendor dependence.

Management is leaning into this opportunity. On the earnings call, CEO Lisa Su highlighted how “agentic AI” workloads — AI systems that act autonomously and coordinate complex tasks — are turbocharging CPU demand alongside GPUs. That trend is particularly important for AMD, which has deep CPU strength and growing GPU capabilities. Upcoming Helios systems already have marquee customers lined up, including large platforms comparable in scale to Apple and other mega‑caps, underlining confidence in AMD’s roadmap.

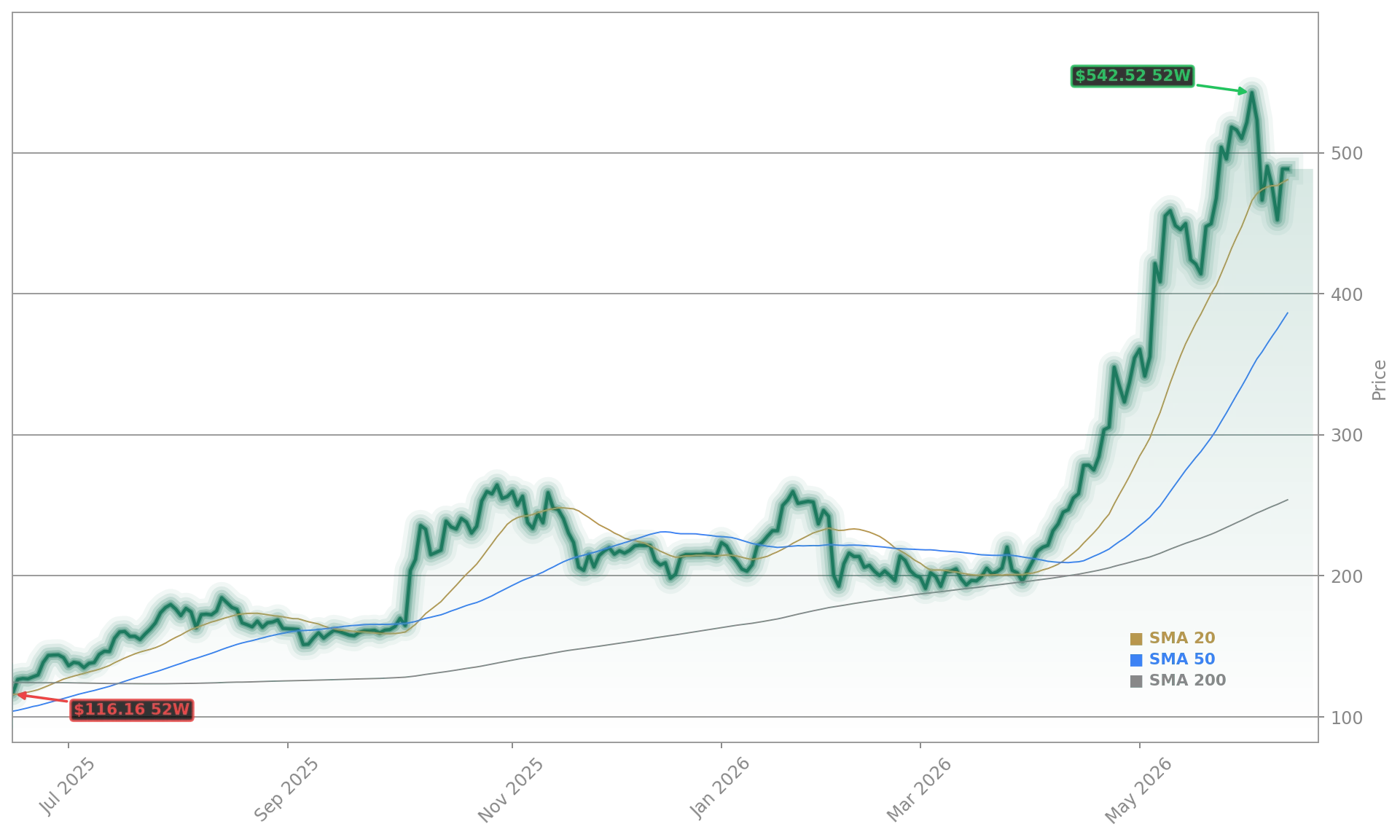

The market backdrop is reinforcing the narrative. Semiconductor analysts now expect the global chip market to top $1 trillion this year as AI data-center buildouts accelerate, helping lift a broad swath of chip names. AMD’s performance has turned it from a laggard into one of 2026’s standout NASDAQ winners, with the stock up more than 100% year to date and roughly 350% over the past 12 months.

How did guidance reframe AMD Earnings?

Forward guidance was another key driver of the AMD Earnings reaction. For Q2 2026, the company is guiding for revenue of about $11.2 billion at the midpoint, implying growth in the mid‑40% range year over year. Within that, AMD expects server CPU revenue alone to climb more than 70% versus the prior year, reflecting both share gains and market expansion as AI‑optimized CPUs become standard in data-center architectures.

Management has also sharply upgraded its long‑term view of the server CPU market. AMD now sees the addressable market growing more than 35% annually to over $120 billion by 2030, almost doubling its prior long‑term growth estimate of around 18%. That revision helps justify aggressive capex and R&D around EPYC and Instinct, but it also raises the bar for execution. Supply constraints, especially in advanced packaging for high‑performance AI chips, remain a key risk that could limit AMD’s ability to fully capitalize on demand in 2026 and 2027.

Despite these challenges, the market’s near‑term takeaway is clear: the latest AMD Earnings suggest the AI data-center cycle has further to run, and AMD is positioned to capture a meaningful slice of that spend alongside rivals like Tesla’s in‑house AI efforts and other hyperscaler initiatives.

Are valuation and analyst views getting stretched?

The flip side of a blowout AMD Earnings report is valuation. At roughly $455 per share, AMD trades at about 150 times trailing earnings and around the low‑40s on a forward price‑to‑earnings basis using consensus 12‑month EPS forecasts. That is a hefty premium to NVIDIA and far above many S&P 500 technology peers.

Technical signals underscore the froth: the relative strength index (RSI) recently pushed above 80, a zone many traders view as overbought. UBS responded by downgrading AMD to “Underperform”, arguing that the risk‑reward has become less attractive in the short term after the parabolic move. Yet other banks are moving the opposite way. Baird lifted its price target to $625, while KeyBanc and TD Cowen raised their targets to around $530 and $500, respectively. Evercore ISI went even further in one of the latest AI‑driven upgrades, setting a Street‑high target near $579, citing AMD’s expanding CPU role in agentic AI workloads.

On Wall Street, this split is feeding a broader narrative of a “changing of the guard” in AI leadership. Recent trading sessions have seen investors rotate some exposure from entrenched winners into names like AMD and Intel, even as valuation concerns mount. For existing shareholders, that means watching position sizes and volatility; for new buyers, it argues for caution and patience despite the impressive AMD Earnings trajectory.

Related Coverage

Investors looking for more context on how AMD Earnings fit into the broader AI trade can explore additional analysis at stocknewsroom.com. A recent deep dive, “AMD Earnings +6.1% Surge as AI Boom Reprices the Stock”, examines an earlier leg of the rally, comparing valuation, growth, and risk factors as the AI narrative accelerated. Reading both pieces together offers a fuller picture of how sentiment has evolved and what could drive the next move.

In summary, the latest AMD Earnings confirm that Advanced Micro Devices, Inc. has firmly established itself as a central player in the AI data-center buildout, even if its stock is now priced for near‑flawless execution. For U.S. investors, the name has become a core way to play the AI infrastructure boom, but one that demands respect for volatility and valuation risk. The next few quarters of AMD Earnings will be critical in showing whether the company can grow into its lofty multiple and sustain its new leadership role in the NASDAQ and broader AI ecosystem.