Are blowout AMD Earnings and a turbocharged AI outlook enough to justify the stock’s explosive after-hours surge?

How did Advanced Micro Devices move the market?

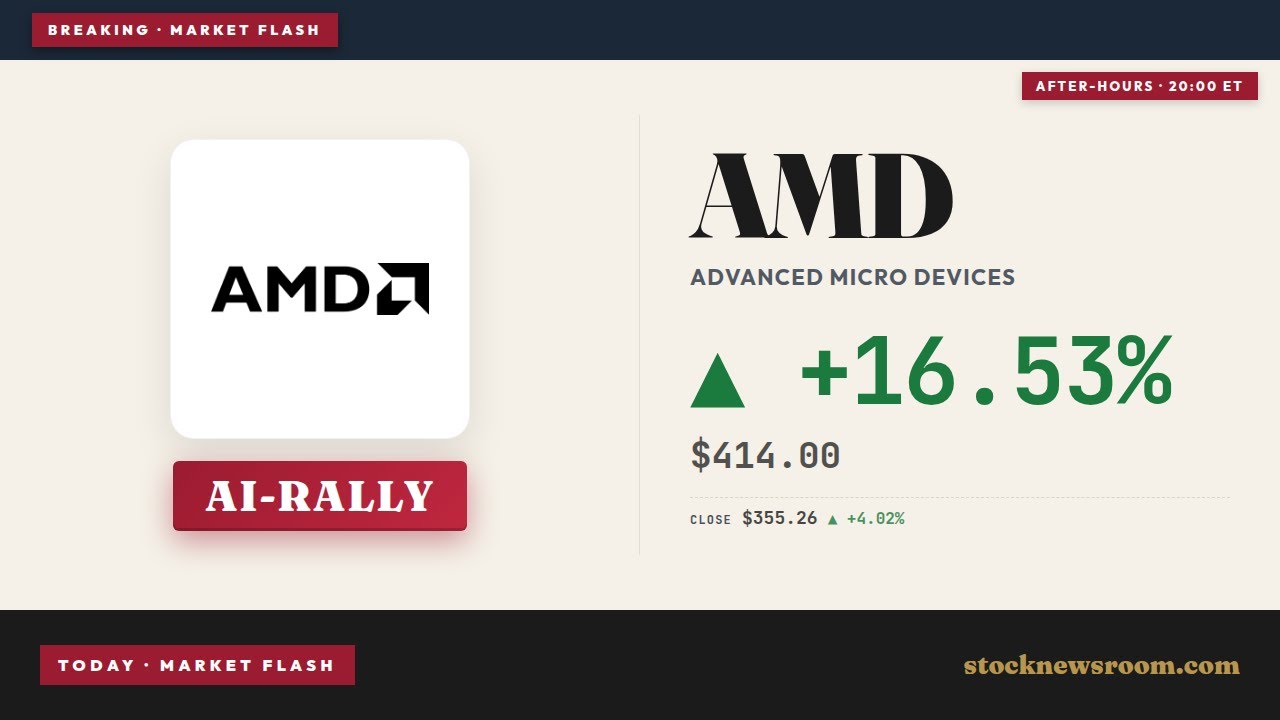

AMD shares closed Tuesday’s NASDAQ session at $355.26, up 4.02% on the day, before exploding to about $414 in late trading, a jump of roughly 16.5%. That move came after the chipmaker reported first‑quarter 2026 numbers that comfortably cleared Wall Street estimates and paired them with a strong second‑quarter outlook. The reaction helped underpin fresh record highs for the S&P 500 and Nasdaq 100, reinforcing how central AI‑linked semiconductor names have become for U.S. equity benchmarks.

With a 52‑week range between $96.88 and $362.79, the after‑hours quote put AMD above its prior one‑year high, underscoring how quickly sentiment has flipped from cautious to outright optimistic. The latest AMD Earnings also triggered notable portfolio moves: ARK Invest, run by Cathie Wood, sold roughly $16.3 million of AMD across several ETFs into the strength, locking in gains after a powerful AI‑driven run.

What do the latest AMD Earnings show?

For Q1 2026, Advanced Micro Devices, Inc. delivered revenue of $10.25 billion, up 38% year over year and ahead of the roughly $9.89 billion analysts had expected. Adjusted earnings per share came in at $1.37, beating consensus estimates near $1.29–$1.28. Operating margin on a non‑GAAP basis improved to about 25%, reflecting the high mix of data‑center business and better scale in AI accelerators and EPYC server CPUs.

The star of the report was the data‑center segment. Revenue there climbed 57% to $5.8 billion, powered by demand for AI‑optimized GPUs and high‑core‑count CPUs used in cloud infrastructure. Management highlighted that every AI accelerator AMD can manufacture is effectively sold, mirroring commentary from rivals like NVIDIA while positioning AMD as a credible second source for hyperscalers such as Microsoft, Meta Platforms and OpenAI. The company also reiterated that its MI‑series accelerators are competitive in both training and inference workloads.

How bullish is AMD’s new guidance?

Alongside the Q1 AMD Earnings beat, management issued a notably upbeat outlook. For the second quarter of 2026, AMD guided revenue to about $11.2 billion, plus or minus $300 million, versus analyst expectations around $10.5–$10.52 billion. At the midpoint, that implies roughly 46% year‑over‑year growth. The company also projected an adjusted gross margin of about 56%, modestly above the Street’s 55.3% forecast, suggesting that AI and data‑center demand is not coming at the expense of profitability.

CEO Lisa Su laid out an even more aggressive longer‑term view on the earnings call, doubling AMD’s estimate of the server CPU total addressable market to more than $120 billion by 2030 as agentic and inference‑heavy AI workloads proliferate. Management now expects the server CPU market to grow more than 35% annually through the decade, versus a prior 18% forecast, and sees AMD’s own server CPU revenue rising more than 70% year over year in Q2 alone. Su said AMD aims to capture over 50% of this expanding server CPU market as new EPYC generations like Turin and Venice ramp.

Where does AMD stand versus NVIDIA and Intel?

For U.S. investors, the key question after these AMD Earnings is how the company stacks up against its closest peers. NVIDIA still dominates the AI accelerator landscape, but cloud providers and large enterprises increasingly want a multi‑vendor strategy. AMD’s MI450 and upcoming “Helios” full‑rack AI systems are designed to offer that alternative, and early customers reportedly include OpenAI and Meta. That dynamic, if sustained, would make AMD a structural beneficiary of the hundreds of billions in capex planned by hyperscalers in the next few years.

At the same time, traditional CPU rival Intel is trying to reassert itself in data centers and AI, including with investments in AI start‑ups and foundry capacity. Yet AMD’s raised server CPU forecast and share gains in high‑performance computing suggest it continues to outgrow Intel in this segment. The company’s R&D spend, about $8 billion in its last full fiscal year, still trails NVIDIA but keeps AMD firmly in the race for next‑generation architectures.

What are the risks for Wall Street portfolios?

Despite the upbeat AMD Earnings, valuation risk is becoming more acute. After the post‑report surge, AMD is trading at roughly 44 times expected earnings, nearly twice the price‑to‑earnings multiple of NVIDIA on some estimates. The stock had already climbed about 74% in April alone, its strongest monthly gain since 2001, and more than tripled over the past year. That kind of momentum leaves little room for execution missteps or a slowdown in AI capex.

Some investors are already trimming exposure. ARK Invest’s sale into strength shows that even long‑term AI bulls are managing position sizes after such a move. For diversified U.S. portfolios heavy in mega‑cap tech and AI semis, concentration risk is a real consideration, especially as chipmakers and infrastructure names like Apple and Tesla increasingly trade as one macro “AI basket.” While no major Wall Street bank issued fresh price‑target changes immediately after the report, prior positive views from firms such as Goldman Sachs and Morgan Stanley now rest on even more ambitious growth assumptions.

Related Coverage

Investors looking for a deeper dive into how AI demand is reshaping the chipmaker’s growth profile can read AMD Earnings Surge: Q1 Beat and AI Boom Ignite Rally. That analysis examines whether the current post‑market spike in AMD’s share price is sustainable and how the data‑center mix might evolve over the coming quarters.

We delivered an excellent first quarter driven by rising AI infrastructure demand, with data center now the primary engine of our revenue and earnings growth.— Lisa Su, CEO of Advanced Micro Devices, Inc.

In summary, the latest AMD Earnings underscore how central AI infrastructure has become to Advanced Micro Devices, Inc., with data‑center chips now the key driver of revenue and profit. For U.S. investors, AMD offers high‑beta exposure to the AI build‑out, but at a valuation that demands continued flawless execution. The next few quarters will reveal whether AMD can translate today’s record backlog and bold server CPU targets into durable earnings power.