Could MicroStrategy really be pushed into selling Bitcoin, or is the market overreacting to balance-sheet stress?

Why are MicroStrategy Bitcoin Sales back in focus?

MicroStrategy Incorporated, now operating as Strategy, holds 843,738 bitcoins, roughly 4% of Bitcoin’s maximum supply, and still aims for 1 million. That scale has long made MSTR a high-beta proxy for Bitcoin, often drawing comparisons with concentrated conviction trades in names like Tesla or NVIDIA. But the key issue now is no longer just accumulation. It is whether liquidity management could force the company into MicroStrategy Bitcoin Sales for the first time in a meaningful way.

The debate intensified after Arca CIO Jeff Dorman argued that the company’s capital structure has become far more fragile. His concern centered on roughly $15 billion of preferred securities carrying about $1.5 billion in annual dividends, layered on top of a business model already tied tightly to Bitcoin price swings. Dorman’s core argument is that if Bitcoin weakens further, management may face a hard tradeoff between preserving cash, supporting preferred holders, and protecting its BTC stack.

What did MicroStrategy signal about selling?

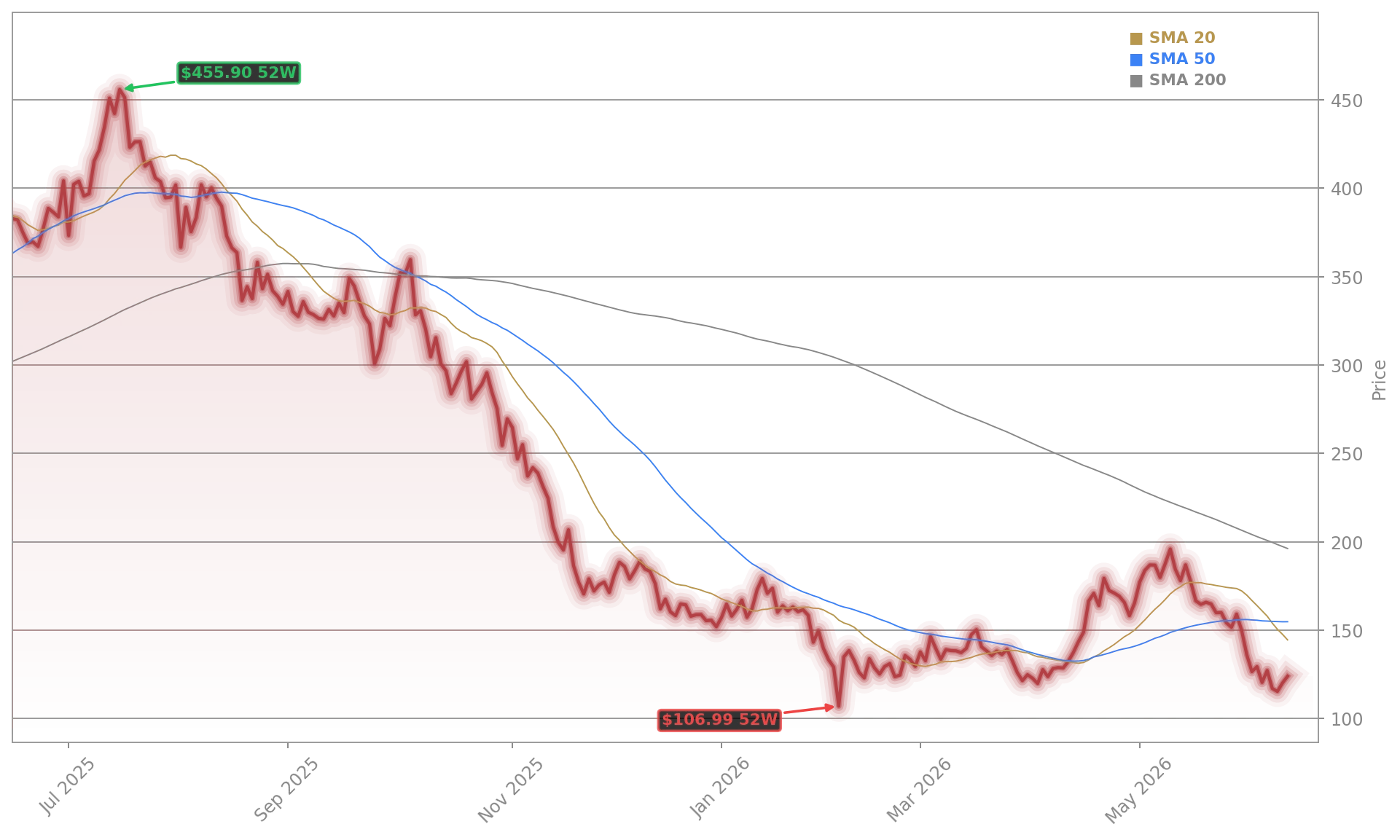

The market was rattled because Michael Saylor recently suggested that partial profit-taking can no longer be ruled out. That marked a notable shift from his long-promoted “buy the top forever” posture. During the company’s Q1 2026 earnings discussion, management acknowledged a harsher financing backdrop after a quarter in which the company posted a $12.54 billion net loss, driven largely by crypto-related valuation pressure.

Recent blockchain-tracked transfers to Coinbase Prime added fuel to the anxiety. One transfer involved about 411.48 BTC, worth roughly $30.3 million. Relative to total holdings, that amount is tiny. Even so, traders interpreted the move as a warning sign that MicroStrategy Bitcoin Sales may no longer be unthinkable. Polymarket-style odds cited by crypto watchers have also surged on the question of whether sales happen before year-end.

Still, the panic may be overstated. The company has technically sold Bitcoin before, unloading 704 BTC in December 2022 before buying back even more two days later. That history matters because it shows tactical sales do not automatically mean the core treasury strategy is ending.

How exposed is MicroStrategy to Bitcoin flows?

Even with its enormous stash, Strategy does not control Bitcoin demand. Estimates in recent market commentary put the company’s share of net Bitcoin inflows at roughly 7% to 9%. That is significant, but nowhere near enough to make Bitcoin structurally dependent on one buyer. For US investors, this means Bitcoin itself is less vulnerable than MSTR equity if financing stress builds.

That distinction matters. MSTR remains a leveraged expression of Bitcoin plus capital-markets engineering, not a simple spot-BTC vehicle like an ETF. It also helps explain why some investors rotate between MSTR and mega-cap names such as Apple when risk appetite changes. TradingView commentary has remained broadly constructive on momentum and institutional demand, while GuruFocus has highlighted warning signals in valuation and financial quality metrics. TradingKey, meanwhile, pointed to bullish analyst sentiment, including a median target of $347.50, though no fresh named calls from firms such as Citigroup or RBC Capital were detailed in the available material.

Can MicroStrategy avoid forced Bitcoin sales?

The bull case is that Saylor again finds a capital-markets workaround. Dorman himself suggested one possibility could be refinancing converts with longer-dated securities, even if Saylor has indicated less enthusiasm for convertibles. Another possibility is pausing or altering preferred dividends rather than selling BTC. Either route would be controversial, but both would be preferable for Bitcoin bulls versus outright liquidation during a weak tape.

Related Coverage: Investors tracking balance-sheet risk should also read this look at MicroStrategy debt reduction and the $1.5 billion paydown warning, which examines whether recent liability management is a smart reset or a sign the Bitcoin machine is slowing. For the broader crypto backdrop, this report on Bitcoin’s plunge and $2.6 billion in ETF outflows explains why sentiment around leveraged Bitcoin proxies has become more fragile across Wall Street.

MicroStrategy Bitcoin Sales remain a risk scenario, not a confirmed shift in strategy. For investors, the next key test is whether MSTR can keep funding its capital structure without sacrificing Bitcoin exposure, because if that balance holds, the stock may remain one of Wall Street’s most explosive crypto-linked trades.

Sell BTC to pay the prefs — bad for MSTR, bad for BTC, good for STRC.— Jeff Dorman

Fazit folgt.