Did Ross Stores just prove bargain retail is still one of the strongest plays in a selective consumer market?

Why did Ross Stores Earnings move shares?

Ross Stores Earnings landed well above expectations, with first-quarter earnings per share of $2.02 on revenue of $6.01 billion. Both figures beat consensus estimates, while total sales rose 21% and comparable store sales climbed a record 17%. That comp gain stood far above what Wall Street had been modeling and signaled broad-based traffic strength rather than a one-off margin surprise.

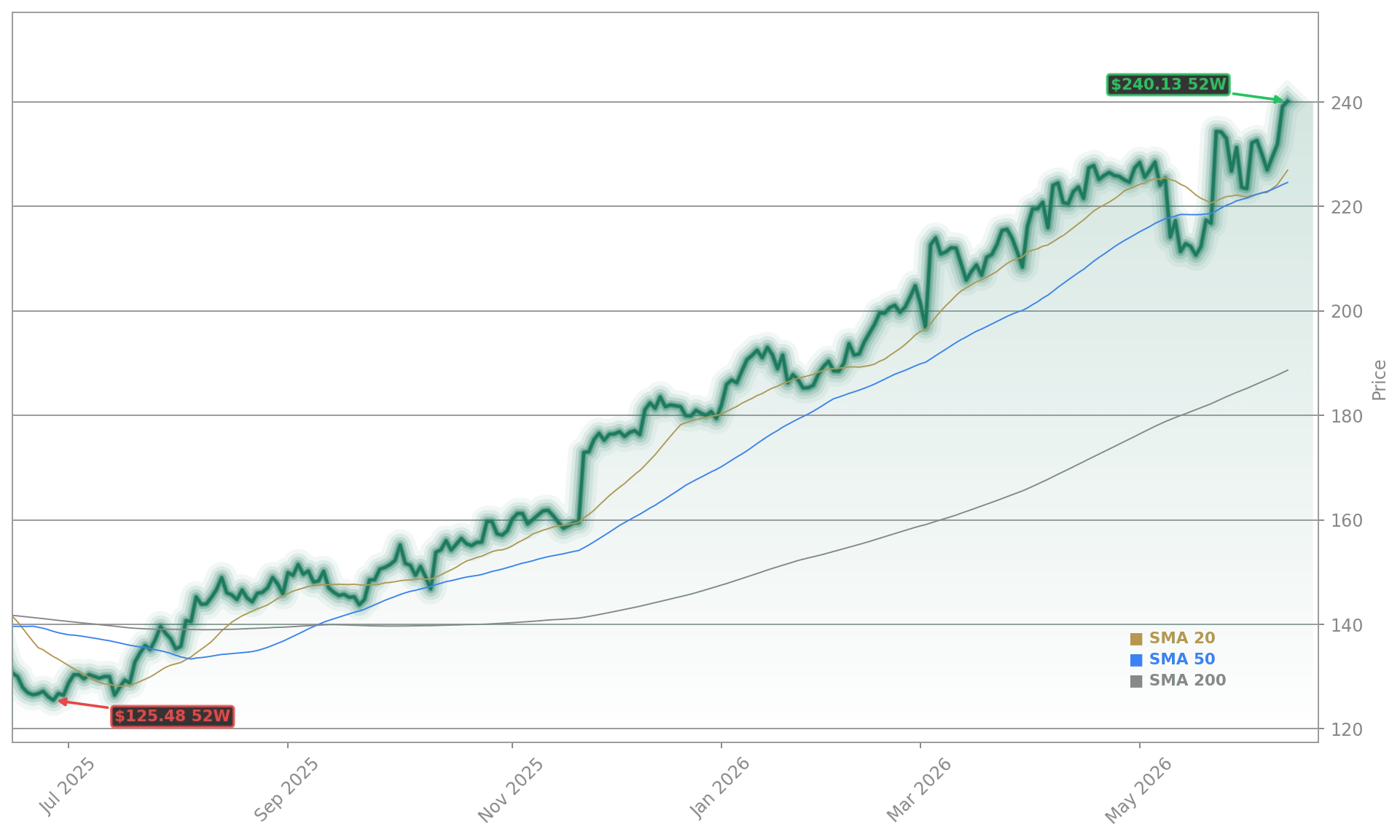

The stock traded at $232.63 Friday, up 7.11% from the prior close of $229.50. MarketBeat reported the move marked a new 52-week high, an important distinction for momentum investors screening retail winners. Management also raised full-year earnings guidance to $7.50 to $7.74 per share and declared a quarterly dividend of $0.445, adding to the upbeat tone around the release.

How does Ross Stores compare with rivals?

The latest numbers strengthen Ross Stores’ position in the off-price retail trade, where value and branded merchandise matter more when consumers stay selective. Rival TJX delivered a strong report earlier in the week, and Ross now appears to be confirming the same theme: shoppers are still spending, but they want sharper prices. That backdrop has helped discount chains outperform many broader apparel names.

For US investors, the read-through matters beyond apparel. A healthy Ross quarter suggests consumer wallets are not shutting down, even if buyers remain focused on deals. That makes the report relevant for investors also watching discretionary leaders like Amazon and Walmart, as well as broader retail demand trends that can influence sentiment around names such as Target. Ross operates Ross Dress for Less and dd’s DISCOUNTS, two banners built for exactly this environment.

What are analysts saying on Ross Stores?

Wall Street reacted quickly to the report. Bank of America raised its price target on Ross Stores to $255 after the earnings beat and higher outlook. Separately, TradingView data highlighted that the average 12-month analyst target moved up to roughly $260.06, versus about $247 previously, reflecting a more constructive stance after the quarter. Across 22 analysts, the stock still leans Buy overall.

Not every observer is fully bullish at current levels. A cautious view from Seeking Alpha argued that Ross is executing well but faces tougher year-over-year comparisons ahead, especially in the second half, and that valuation now looks less forgiving near 25 to 26 times forward earnings. That debate is typical after a sharp post-earnings rally: fundamentals improved, but expectations have risen as well.

What comes next for Ross Stores?

Management’s guidance increase is the clearest near-term catalyst, because it suggests confidence that recent momentum will not disappear immediately. The company is also continuing store expansion, with plans for about 110 new stores this year, while maintaining a $1.275 billion stock repurchase program for 2026. Those capital allocation choices indicate Ross still sees room to grow both its footprint and shareholder returns.

Ross Stores Earnings also add an important data point for the broader market. Investors have been weighing whether the US consumer is weakening or simply becoming more selective. Ross supports the second view. In a market where traders often chase high-growth tech names like NVIDIA and Apple, steady execution from an off-price retailer can still matter for diversified portfolios. If traffic trends remain strong, Ross may keep standing out as one of the cleaner defensive growth stories in consumer discretionary.

Ross Stores Earnings delivered exactly what bulls wanted: a decisive beat, a higher outlook, and proof that off-price retail remains a sweet spot in the current consumer backdrop. For investors, the key question now is whether elevated expectations can be matched over the next two quarters. If Ross keeps converting bargain hunting into traffic and earnings growth, the stock could remain a retail leader through 2026.

Fazit folgt.